The world armaments market is gradually changing towards more competition, mainly due to the emergence of new exporters and the policy of diversification of overseas suppliers pursued by major importers like India. There is also an increasing demand from Asian and Arab buyers to create their own military-industrial infrastructures by buying technology and localizing production.

This situation can become a good opportunity for increasing the number of Russia's partners in the world market of arms and military equipment, especially in the segment of naval shipbuilding.

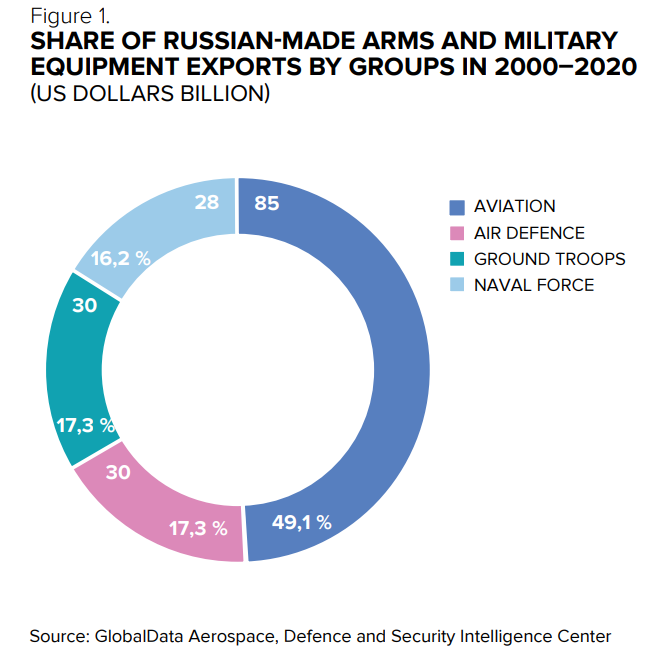

Military-technical cooperation (MTC) generates annually essential cash flows for the defense industry (more than $15 billion) and has also the highest margin (in comparison with the State Armament Program and consignment of civilian products). For the period of 20 years – from 2000 to 2020 – the Rosoboronexport (ROE) supplied weapons and military equipment worth more than $180 billion to foreign customers. According to General Director of Rosoboronexport Alexander Mikheev, aircraft building products accounted for the main volume of deliveries – over $85 billion, and more than $30 billion for each air defense and equipment for land forces. The volume of weapons and military equipment for the Navy was about $28 billion (Fig. 1).

As it follows from Rosoboronexport’s data, in terms of exports the naval equipment segment still lags behind the aviation, air defense, and ground forces.

At present, the structure of the orders’ portfolio for Russian-made weapons and military equipment is as follows: at the end of 2020, the total volume amounted to $53.8 billion. The volume of orders for naval products reaches $5.5 billion, which is equivalent to about 10.2% of the total portfolio. There are contracts for supply and joint construction of ships and submarines, as well as supply of various weapons for them, coastal support equipment, and infrastructure projects.

There is information on one contract for warship construction: four modernized frigates of project 11356 worth $3.08 billion, two of which will be produced at Yantar Shipyard by 2023 and the other two – at Goa Shipyard Limited, India. Thus, about 44% of the naval portfolio may be formed at the expense of ship borne armaments, coastal facilities, etc.

The strong point of the domestic shipbuilding industry is its high scientific and technical potential and its fuller implementation, including joint projects with foreign partners. This can lead to a considerable growth of sales in the field of military-technical cooperation. There are other serious prerequisites for development. First of all, we should note the favorable price-quality ratio offered for foreign customers and their willingness to transfer technology, as well as the high brand recognition, in particular, that of the world bestseller – the Varshavianka.

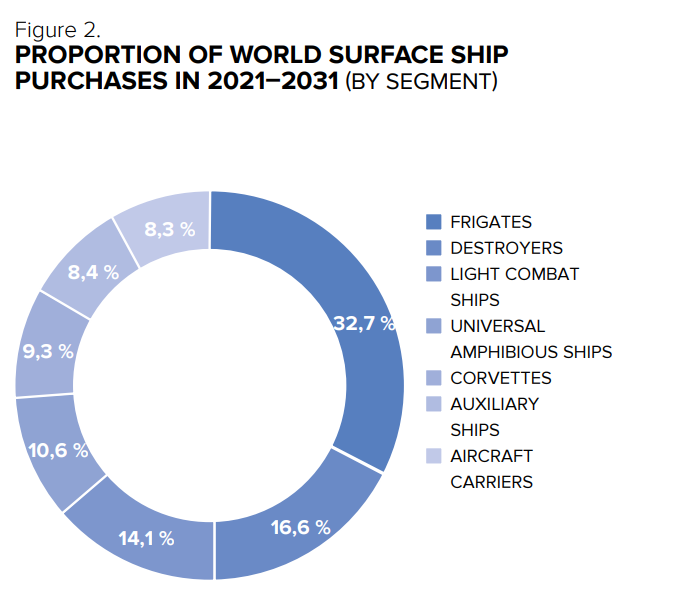

An equally important factor for increasing exports is the favorable market environment for the next decade. GlobalData analysts estimate the Compound Annual Growth Rate (CAGR) of the world market of naval ships and surface ships in 2021–2031 to be 3.49%: the volume will increase from $34.1 billion to $48.7 billion. Frigates will become leaders in terms of purchases’ volume with a share of about 32.7% in the following 10 years (Fig. 2). It should be noted that the highest growth rate of this segment is expected in India, with a CAGR'31 of 6.4%.

One of the opportunities favorable to Russian shipbuilders is to focus on meeting the growing demand for frigates imports, including orders from India.

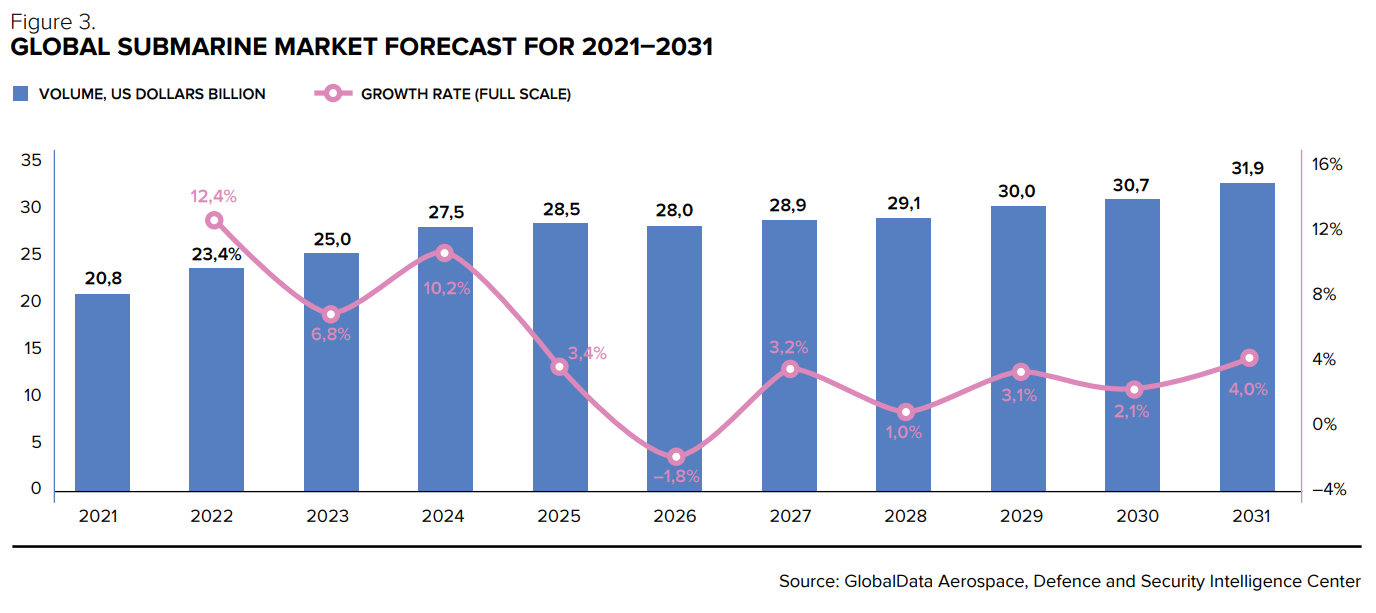

GlobalData experts also expect an active development of the global submarine market. According to their forecasts, the CAGR in 2021–2031 will reach about 4.36% and the volume will increase from $20.8 billion to $31.9 billion (Fig. 3).

India will also be one of the main buyers of submarines. It is estimated that New Delhi can spend about $23.5 billion over the next 10 years to acquire nuclear and diesel-electric submarines. At that, 63% ($14.8 billion) will presumably be spent on submarine programs and 37% ($8.7 billion), on nuclear submarines.

The Indian government announced a tender for the construction of six non-nuclear Project-75I submarines worth $5.4 billion. The Defense Ministry's request for proposals was sent to two Indian companies: Mazagon Dock Shipbuilders Limited (MDL) and Larsen & Tubro (L&T).

The Russian United Shipbuilding Corporation (USC) competes with four global players: German TKMS, French Naval Group, Spanish Navantia, and South Korean DSME. The competition is going to be serious: the tender accounts for almost a quarter of India's total planned expenditure on submarines over the next 10 years. USC's main trump cards are its successful experience in building naval equipment for India and its readiness for extensive cooperation under the “Make in India” program.

If the holding can create a quality offer in the frigates and submarines segment and focus on the Asia-Pacific region, and India in particular as a key geographic area, winning the tender for Project-75I submarines will become the first step towards building a large order book and increasing cash flow from exports.

Author: Sasha Makarov

©New Defence Order. Strategy №1 (72) 2022